Corporate tax rates play a pivotal role in shaping economic landscape and tax policy debate, particularly as the discussion surrounding the Tax Cuts and Jobs Act (TCJA) unfolds. Enacted in 2017, the TCJA dramatically altered corporate tax rates, slashing them from 35% to 21% in hopes of spurring economic growth and increasing corporate tax revenue. As Congress prepares for upcoming decisions relating to these tax policies, stakeholders are divided; some advocate for raising corporate tax rates to fund social programs, while others argue for further cuts to enhance investment and job growth. The TCJA impacts continue to be scrutinized, as analysts weigh the short-term benefits against the long-term implications of reduced tax revenues. As the political landscape shifts, the implications of corporate taxation will remain a central issue in economic discussions and future legislative agendas.

In economic discussions, corporate taxation refers to the levies imposed on corporate profits, influencing business behavior and capital allocation. The modification of these tax rates, highlighted by the landmark Tax Cuts and Jobs Act of 2017, marks a significant shift in the American fiscal landscape. Debates on tax reform often focus on how changes affect both economic growth and the overall revenue generated from corporate taxation. As political factions vie for influence, the broader implications of these changes are becoming more evident, drawing attention to both potential revenue streams and the impact on national growth. The ongoing discourse reflects a careful balancing act between fostering a favorable investment climate and securing necessary tax revenue for public services.

Impact of the Tax Cuts and Jobs Act on Corporate Tax Rates

The Tax Cuts and Jobs Act (TCJA), enacted in 2017, significantly transformed corporate tax rates in the United States. One of its primary objectives was to reduce the corporate statutory rate from 35% to 21%. This marked a historic shift in tax policy, designed to enhance the attractiveness of the U.S. for business investment amidst a globally competitive corporate environment. Advocates of the TCJA argued that such reductions would stimulate economic growth by encouraging firms to reinvest profits back into their operations, thereby driving job creation and wage increases. However, the anticipated benefits of these tax cuts have sparked considerable debate in the political arena, with Republicans frequently championing them as a catalyst for growth while Democrats caution against the potential fiscal repercussions, particularly a significant drop in corporate tax revenue.

Despite the initial intentions behind the TCJA, the actual impacts on corporate tax revenue have proven more complex. As Gabriel Chodorow-Reich and his co-authors noted in their analysis published in the *Journal of Economic Perspectives*, although corporate tax revenue did experience a sharp decline after the TCJA’s implementation, it began to recover in subsequent years. This recovery was likely fueled by rising business profits that exceeded projections, raising questions about the long-lasting effects of the TCJA on corporate taxation. This aspect has become a focal point in ongoing discussions regarding tax policy, especially as some lawmakers advocate for reinstating higher tax rates to balance the budget and address social spending needs. Understanding these trends is vital as Congress prepares for another round of tax negotiations.

Debate Over Corporate Tax Revenue and Economic Growth

The economic implications of the TCJA have sparked a robust debate among policymakers and economists. Critics argue that the reductions in corporate tax rates have not translated into the substantial wage increases and investment that proponents promised. Chodorow-Reich’s analysis pointed to a modest increase in investment attributed to the TCJA, but emphasized that these gains were insufficient to offset the significant reductions in tax revenue. This reality raises questions about the long-term sustainability of tax cuts as a strategy for economic growth. While some companies reported increased capital expenditures, the overall fiscal health of the government was compromised, leading to concerns about whether the TCJA truly fulfilled its promise to stimulate robust and equitable economic growth.

Additionally, the implications of the TCJA extend beyond simple fiscal measures; they influence the broader tax policy debate in the U.S. As the expiration of certain provisions looms in 2025, questions regarding the appropriate level of corporate taxation have emerged. The disagreements largely focus on what constitutes a fair tax burden for corporations and how to effectively stimulate economic growth without jeopardizing essential public services. The resurgence in corporate profits has made this debate even more contentious, with arguments centering on how much of those profits should be redistributed back into government coffers through taxation. This complex interplay between corporate tax policy, economic growth, and equitable revenue generation underscores the critical nature of ongoing discussions as lawmakers consider adjustments in future tax legislation.

The Challenge of Balancing Corporate Tax Policy

As the expiration of TCJA provisions draws near, Congress faces the formidable task of creating a balanced corporate tax policy that fosters growth while ensuring adequate revenue generation. Supporters of raising corporate tax rates, like Vice President Kamala Harris, argue that increased taxation is necessary to fund critical initiatives such as educational programs and social welfare. In contrast, proponents of further tax cuts maintain that sustaining low corporate rates is essential to foster business investment and stimulate economic dynamism. This conflict highlights the crucial question: How can lawmakers find common ground in navigating corporate tax policy to achieve both revenue adequacy and economic growth?

In light of recent findings that link capital investment more significantly to expensing provisions rather than statutory rate cuts, researchers like Chodorow-Reich suggest a potential compromise. They propose that lawmakers consider reinstating favorable provisions for capital expenses while cautiously increasing corporate rates. This could allow firms to enjoy targeted tax incentives that effectively spur growth, while also increasing revenues needed for public services. Navigating this multifaceted issue calls for thoughtful deliberation and an empirical approach, aiming to reconcile the differing viewpoints while crafting tax policies that foster both corporate responsibility and economic resilience.

Assessing Wages in Relation to Corporate Tax Cuts

One of the most contentious areas of discussion surrounding the TCJA is the relationship between corporate tax cuts and wages. Initially, projections made by the Council of Economic Advisers suggested that wage increases could range dramatically between $4,000 to $9,000 per employee as a result of the TCJA. However, studies conducted by Chodorow-Reich and his colleagues revealed that the actual impact on wages was significantly less, estimating an increase closer to $750 annually in 2017 dollars. This discrepancy raises critical questions about the efficacy of tax policy in directly influencing wage growth, prompting further investigation into how corporate behavior responds to tax incentives and economic conditions.

The findings of modest wage increases suggest that while corporate tax policy can influence business decisions, the relationship is not as straightforward as proponents of the TCJA might argue. Many economists advocate a more comprehensive view that includes factors such as workforce dynamics, market conditions, and overall economic health when evaluating the effects of corporate tax rates on employee compensation. This nuanced understanding is vital as policymakers gear up for upcoming legislative battles in 2025, where wage growth and its connection to tax policy will likely be a central theme of debate. Addressing these issues thoughtfully could pave the way for more effective and equitable tax solutions.

The Future of Corporate Tax Policy

With the expiration of several key provisions of the TCJA on the horizon, the future of corporate tax policy is under intense scrutiny. Economists and lawmakers alike are calling for a reevaluation of the existing tax framework to ensure it aligns with the current economic landscape and addresses the needs of all stakeholders. As companies report record profits, the question arises of how much these corporations should contribute back to societal needs through higher taxation. This is particularly pressing in an era where public resources are stretched thin, and there is a growing expectation for corporations to participate more equitably in funding essential services.

Furthermore, the debate is not solely about raising rates; it also involves the effectiveness of different tax incentives that can spur innovation and growth. Lawmakers are contemplating options such as reinstating full expensing provisions that are more directly linked to driving investment instead of relying solely on rate cuts. The ongoing discussions around corporate tax policy highlight the bigger challenge of crafting a system that supports sustainable economic growth while providing the necessary resources to manage the public good. As both parties prepare for upcoming elections, the stakes in this debate will likely remain high, influencing the trajectory of America’s economic future.

Evaluating the Effectiveness of Tax Cuts and Economic Growth

The TCJA is often presented as a pivotal moment in U.S. fiscal policy, shifting the corporate tax landscape from a relatively high to a competitive low rate. However, the subsequent economic performance has led many economists to evaluate the effectiveness of these cuts critically. While proponents assert that lower corporate rates result in increased investments and, ultimately, job creation, empirical analysis suggests a more complicated reality. As highlighted by Chodorow-Reich, the modest uptick in investments does not necessarily correlate to the expansive growth anticipated by supporters of the TCJA. This discrepancy ignites further discussion about the tax policy’s actual efficacy in stimulating economic growth and enhancing the quality of life for American workers.

As lawmakers head into the next round of negotiations, they will need to address the complexities highlighted by these analyses, balancing the narrative surrounding corporate tax rates with actual economic outcomes. There is a strong argument for policy adjustments that not only maintain competitive tax rates but also harness the potential of strategic tax incentives that can evolve alongside economic conditions. Such a balanced approach could lead to greater investment in future workforce development, a key factor in driving productivity and sustainable economic success for the nation. Emphasizing data-driven policymaking in these discussions will be crucial as they formulate tax solutions that encourage robust economic growth while also safeguarding public interests.

Corporate Tax Cuts and the Increasing Global Competition

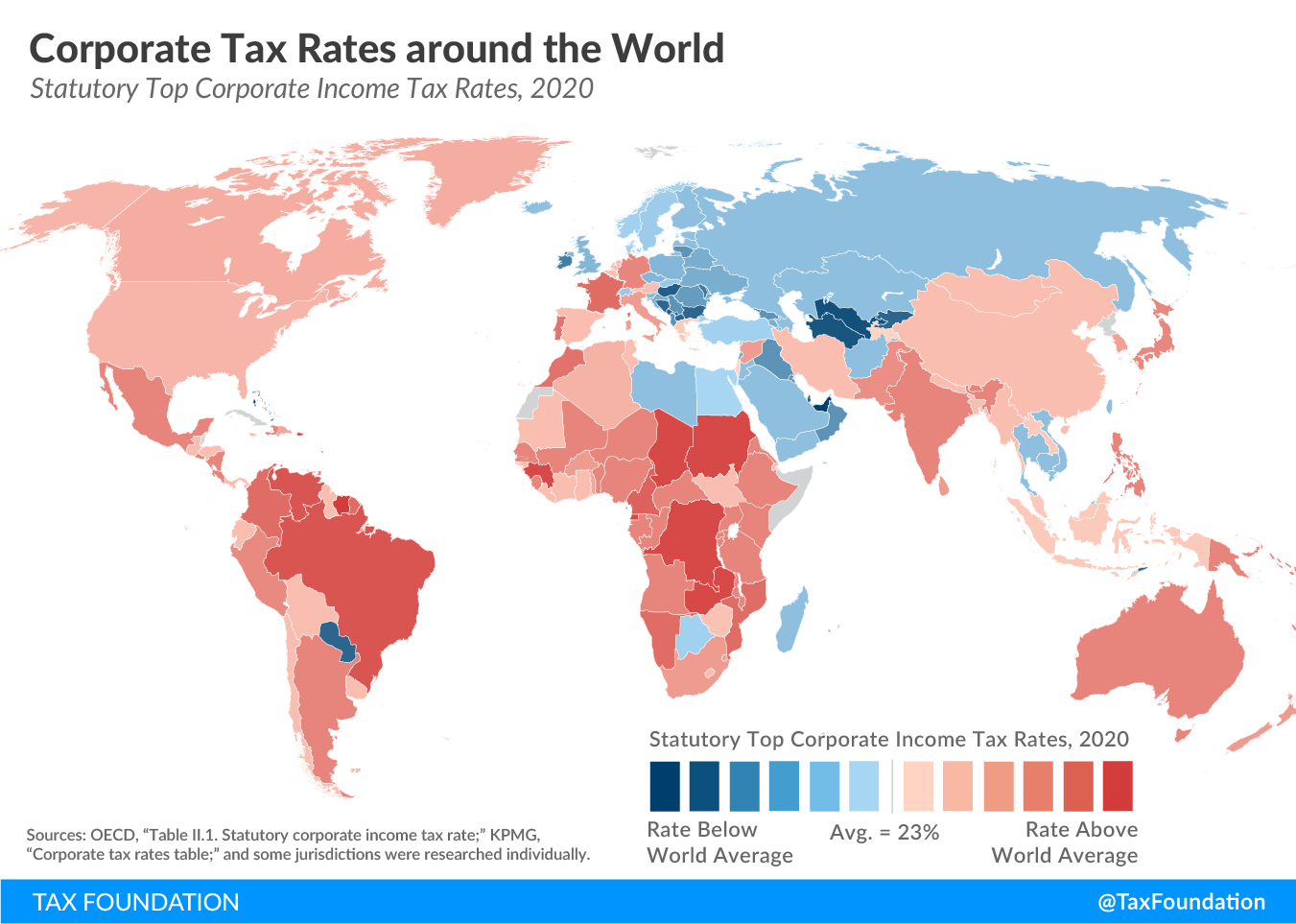

In the wake of the TCJA and its substantial reduction in corporate tax rates, there has been heightened competition among nations to attract business investments. As noted by Chodorow-Reich, prior to the TCJA, the U.S. corporate tax rate positioned it at one of the highest levels globally. The tax law aimed to counterbalance this by making the U.S. more inviting for domestic and foreign corporations alike. Nevertheless, this strategy raises significant questions about how effective such tax cuts can be in light of global economic dynamics, where countries continuously adjust their tax policies to remain competitive.

The influence of international tax competition cannot be understated, particularly as countries pursue lower tax rates to gain a foothold in the global marketplace. This situation places immense pressure on U.S. lawmakers to not only consider the implications of corporate tax rate adjustments at home but also assess how these changes resonate on a global scale. As corporations pivot towards countries with more favorable tax incentives, the United States must grapple with developing a tax policy that strikes a balance between fostering a competitive environment for businesses and ensuring sufficient revenue generation for public goods. The interplay between corporate taxation and international competitiveness will undoubtedly shape the landscape of future economic policies.

Challenges in Tax Policy Debate and Public Perception

The discussion around corporate tax policy is not only a legislative matter but also deeply entwined with public sentiment and perceptions of fairness. As the expiration of TCJA provisions approaches, public understanding of tax policy impacts becomes critical in shaping potential reforms. Proponents of increasing tax rates argue that corporations benefit from societal infrastructure, which should be fairly funded through taxation. Conversely, businesses argue that high taxes stymie growth and that job creation is the best form of tax revenue. This dichotomy complicates the tax policy debate, as policymakers must navigate these differing viewpoints while crafting equitable solutions that facilitate both economic growth and necessary government funding.

To effectively address these challenges, stakeholders must engage in transparent dialogues about the implications of tax policies on various segments of the economy. Providing clear communication regarding how corporate tax revenue supports public services can help bridge the understanding gap between corporations and the public. Moreover, engaging economists and financial experts to analyze the real impacts of the TCJA can inform future tax strategies that seek a balance between incentivizing business endeavors and ensuring robust government funding. Shifting the focus of the tax policy debate towards collaborative and data-driven discourse could lead to more sustainable outcomes beneficial for both corporate interests and the greater public good.

Exploring Long-Term Implications of Tax Cuts

As lawmakers gear up for the significant legislative sessions in the coming years, the enduring effects of tax cuts enacted under the TCJA cannot be ignored. Evaluating these long-term implications is vital for informed decision-making going forward. While tax cuts are often viewed as immediate boosts to business, it is crucial to understand that they may lead to long-term consequences for federal revenue and economic stability. The unexpected recovery in corporate tax revenues following the TCJA’s initial drop invites further exploration into the factors contributing to this resurgence, emphasizing the importance of empirical data in shaping future tax policy.

Furthermore, as the economy continues to evolve with emerging technologies and global shifts, the corporate tax framework must adapt accordingly. Policymakers should consider innovative approaches that balance the need for competitive tax rates with the necessity of generating adequate revenue. Engaging various economic stakeholders, including businesses, employees, and the public, can foster a more comprehensive understanding of how tax policies influence overall economic health. By taking proactive measures to assess the long-term implications of the TCJA, legislators can craft a tax policy landscape that not only supports immediate growth but also lays a foundation for a resilient and equitable economic future.

Frequently Asked Questions

How do corporate tax rates impact corporate tax revenue under the Tax Cuts and Jobs Act?

The Tax Cuts and Jobs Act (TCJA) significantly lowered corporate tax rates from 35% to 21%, leading to a projected annual decline in federal corporate tax revenue by $100 billion to $150 billion over ten years. Nevertheless, corporate tax revenue began to recover in 2020 as business profits exceeded expectations, suggesting that lower rates could stimulate initial growth but may not fully compensate for revenue losses in the long term.

What are the economic implications of raising corporate tax rates in the context of the TCJA?

Raising corporate tax rates may provide additional revenue to fund public initiatives while also affecting business investments. Research shows that corporate tax policies can directly influence investment decisions; therefore, reinstating higher tax rates combined with targeted expensing provisions could strike a balance that encourages growth while increasing necessary tax revenues.

What role did the TCJA play in the debate over corporate tax rates?

The TCJA triggered significant debate regarding corporate tax rates, with proponents arguing that lower rates foster economic growth by encouraging investment. In contrast, critics highlighted the substantial drop in corporate tax revenue and raised concerns about the long-term impacts on fiscal health and income distribution, suggesting a careful reevaluation of tax policy is necessary as key provisions start expiring in 2025.

How did the corporate tax rate changes influence business investments after the TCJA?

Following the implementation of the TCJA, there was a modest increase in capital investments by corporations, estimated at around 11%. While the law’s tax rate cuts aimed to stimulate investments, analyses indicated that accelerated expensing provisions had a more pronounced effect on driving corporate investment than the statutory rate reductions.

Can raising corporate tax rates affect wages, and how is this linked to the TCJA?

The relationship between corporate tax rates and wages is complex. Although the TCJA intended to increase wages by encouraging more investment, studies yielded only modest wage growth of approximately $750 per year per full-time employee. Raising corporate tax rates, combined with robust investment incentives, could positively impact wages by necessitating increased hiring in response to more capital investments.

How do global corporate tax rate trends relate to the U.S. corporate tax rate changes under the TCJA?

Prior to the TCJA, the U.S. had among the highest corporate tax rates in developed countries. The act brought rates down significantly, aligning the U.S. with international trends where many nations had lowered their rates to remain competitive. However, as discussions of revising the TCJA emerge, there remains a need to consider how such changes would affect the U.S.’s global tax competitiveness and investment attractiveness.

| Key Points | Details |

|---|---|

| Upcoming Tax Debate 2025 | Congress is preparing to revisit the 2017 Tax Cuts and Jobs Act as major provisions will expire, stirring partisan debates. |

| Corporate Tax Cuts Stakes | Renewal of corporate tax cuts is crucial as it significantly impacts federal revenue and voter priorities. |

| Economic Impact Analysis | The analysis indicates modest wage increases and business investments following the corporate tax cuts, yet, tax revenue dropped significantly. |

| Partisan Perspectives | Republicans advocate further cuts for growth, while Democrats propose increasing rates to fund social programs. |

| Long-term Revenue Projections | The TCJA is projected to decrease federal corporate tax revenue by $100-150 billion annually. |

| Investment Response to Tax Policy | Firms responded positively to immediate expensing provisions rather than conventional tax rate cuts. |

| Predictions on Wage Increases | Wage growth estimates post-TCJA were overestimated; actual increases were significantly lower. |

| Corporate Tax Revenue Recovery | After an initial drop, corporate tax revenue began recovering, exceeding expectations during the pandemic. |

Summary

Corporate tax rates are pivotal in the current political and economic landscape as Congress gears up for a tax battle in 2025. The 2017 Tax Cuts and Jobs Act significantly reshaped the corporate tax framework, offering deep cuts that have led to positive responses in investment but a drastic reduction in tax revenue. As lawmakers debate the merits of raising or lowering these rates, understanding their historical impacts and economic ramifications is crucial for informed policy decisions. Ultimately, any alterations to corporate tax rates will have far-reaching consequences for both businesses and the economy.