The recent Fed rate cut marks a significant shift in monetary policy, with the Federal Reserve lowering key interest rates for the first time in four years. This reduction is intended to stimulate economic growth by making borrowing cheaper, which can positively impact mortgage rates and help elevate housing affordability. As interest rates wane, consumers might find relief from high credit card debt and other financial burdens, paving the way for increased spending and investment. Fed Chairman Jerome Powell underlined that this strategic move is aimed at balancing economic growth while managing inflation. For many Americans, this cut could mean the difference between struggling under debt and enjoying newfound financial freedom.

In light of the recent decision by the Federal Reserve to reduce borrowing costs, we’re witnessing a pivotal moment for the economy and everyday consumers. This monetary easing is expected to have a ripple effect across various financial sectors, including personal loans, credit lines, and housing markets. With reduced interest rates, individuals seeking home loans will find enhanced accessibility, potentially improving the current housing affordability crisis. Moreover, the outlook on credit card fees and personal debts may become more favorable, offering consumers a respite from high repayment costs. Ultimately, these policy adjustments are designed to foster a more robust economic environment for all.

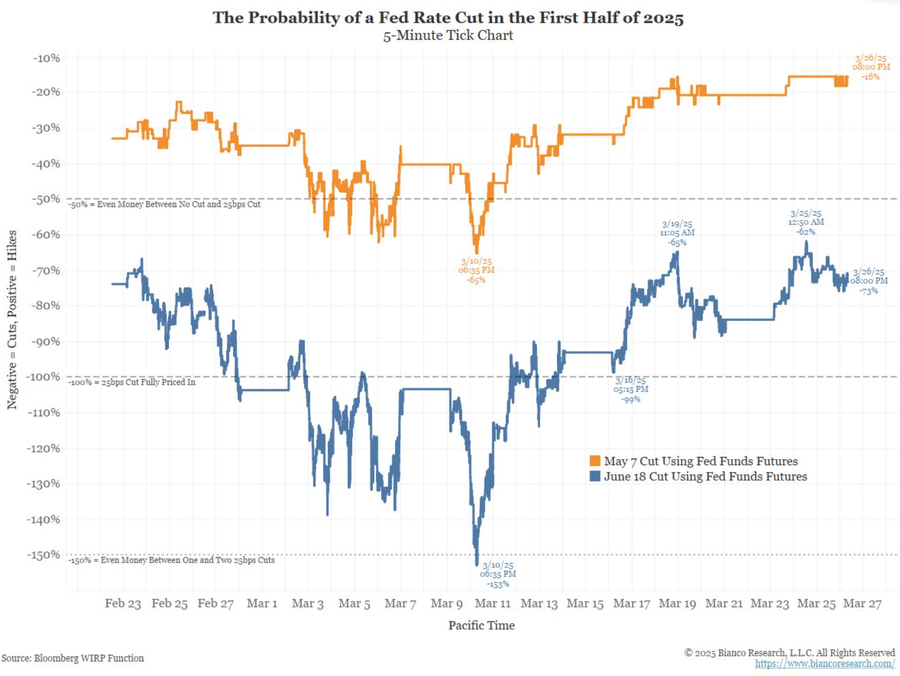

Understanding the Fed Rate Cut and Its Implications

The recent decision by the Federal Reserve to lower interest rates by half a percentage point marks a significant moment for the economy, especially for consumers. This move, the first in four years, is aimed at reducing the cost of borrowing across various sectors. Economists suggest that this reduction will not only aid those with existing credit card debt but will also benefit homebuyers looking for more affordable mortgage rates. As Fed Chairman Jerome Powell highlighted, the U.S. economy remains strong, which makes this cut a strategic response to bolster economic growth and maintain consumer confidence.

The implications of the Fed rate cut extend beyond immediate relief. While consumers can expect some immediate benefits, the broader effects on economic growth and housing affordability will unfold over time. As borrowing costs decrease, households may find it easier to manage their debts, particularly high-interest credit card balances and auto loans. Additionally, the expectation is that mortgage rates will continue to decline, aiding first-time buyers and those looking to refinance. However, the impact will vary based on market reactions and the overall economic climate in the coming months.

Impact of the Fed Rate Cut on Mortgage Rates

One of the most immediate effects of the Fed rate cut is anticipated to be on mortgage rates. Economists have noted that as the Fed eases its monetary policy, mortgage rates are likely to trend downward. This shift could provide vital support for housing affordability, which has been a pressing issue for many Americans. With mortgage rates currently higher than desirable, the rate cut signals a positive trajectory, potentially allowing more families to access the housing market without exorbitant financial strain.

However, while the expectation is for mortgage rates to decrease, it is essential to recognize that these changes may not be instantaneous. The market factors in various elements when determining mortgage costs, including expectations about future interest rates and economic stability. Therefore, while the Fed’s actions aim to lower borrowing costs, consumers must also prepare for a gradual adjustment in mortgage rates, which may take some time to materialize fully.

Consumer Debt Management Following Fed Rate Cuts

The recent rate cut by the Federal Reserve offers a glimmer of hope for consumers grappling with rising credit card debt. Many individuals have been struggling to manage their finances, particularly as interest rates soared in recent years. As the Fed lowers rates, consumers may find relief in the form of lower interest rates on various types of debt. This includes not only credit cards but also car loans and personal loans, all of which can become more manageable as overall borrowing costs decline.

That said, the timeline for meaningful relief remains uncertain. While the current rate cut is advantageous, credit card interest rates are influenced by more than just the Fed’s benchmark rate. Factors such as personal credit risk and market expectations play significant roles. Therefore, while consumers should begin to see some easing over the next year, significant hurdles may still exist, including the residual effects of high rates from previous years and underlying economic volatility.

Long-term Economic Growth Post Fed Rate Cut

Looking beyond immediate consumer benefits, the Fed rate cut is designed to stimulate long-term economic growth. By reducing the cost of borrowing, the Fed aims to encourage spending and investment, which are critical components of a thriving economy. As businesses recognize lower financing costs, they may be more inclined to invest in expansion and job creation, fostering a more robust economic environment. This ripple effect can lead to increased consumer spending, which further bolsters growth.

Nonetheless, the path to recovery is nuanced. While lower interest rates can foster growth, economists caution against potential pitfalls, including inflationary pressures that may arise if growth accelerates too quickly. Monitoring inflation will be crucial as the economy navigates these changes, ensuring that the benefits of the Fed’s action do not lead to instability. Hence, while the Fed’s decision is a step toward economic revitalization, its long-term success hinges on careful management of the ensuing economic landscape.

Addressing Housing Affordability Through Fed Actions

Housing affordability has emerged as a crucial issue for many American families, and the Fed’s recent rate cut is poised to play a significant role in addressing this challenge. As mortgage rates decrease, the hope is that it will alleviate some of the financial burdens faced by would-be homeowners and renters alike. Lower borrowing costs can create opportunities for first-time homebuyers to enter the market, potentially stabilizing housing supply and prices.

However, while the rate cut is a step in the right direction, experts emphasize that it alone will not solve the housing affordability crisis. Structural issues, such as limited housing inventory and sky-high prices in many markets, remain significant barriers. The Fed’s actions can provide temporary relief, but comprehensive solutions must also focus on increasing the supply of affordable housing and addressing income disparities to ensure long-term stability in the housing market.

Exploring the Link Between Economic Growth and Interest Rates

The relationship between interest rates and economic growth is complex but vital to understanding the broader economic landscape. Lower interest rates typically stimulate spending and investment, which can accelerate economic growth. The recent Fed rate cut is expected to enhance this dynamic, encouraging businesses to take on more projects and consumers to spend more freely, resulting in a healthier economy. When interest rates fall, the cost of not just mortgages but also business loans decreases, leading to increased economic activity.

However, economists warn that while reducing rates can spur growth, it must be balanced with the risk of overheating the economy. If lowered rates lead to excessive spending without a corresponding increase in production capacity, inflation could rise, negating the benefits. Therefore, it is vital for policymakers to monitor these trends closely and adjust monetary policy as necessary to maintain sustainable growth without destabilizing the economy.

The Future of Credit Card Debt in a Lower Interest Environment

As the Fed cuts rates, consumers with credit card debt may finally see a pathway to more manageable payments. Credit card interest rates are generally sensitive to changes in the economy, and as the Fed signals a shift towards lower rates, this could translate to relief for consumers who have experienced high interest costs. The expectation is that over time, as the Fed continues its easing policy, credit card providers will adjust their rates accordingly, giving borrowers a much-needed reprieve.

While consumers can anticipate lower rates, it’s important to approach this situation with caution. Many individuals have learned the hard way about the dangers of accumulating debt, especially when interest rates are high. As borrowing costs decrease, widespread financial literacy remains crucial. Consumers should still exercise prudence and create sustainable repayment plans to avoid falling back into debt cycles, ensuring that the benefits of the Fed’s actions translate into real financial freedom.

Potential Future Rate Cuts: What to Expect

Looking ahead, the Fed has indicated the possibility of further rate cuts, which could significantly influence various economic sectors. If the Fed follows through with additional cuts, consumers could experience more relief from financial burdens, particularly regarding mortgages and personal loans. Such measures would likely enhance consumer confidence and stimulate economic activity as people feel more empowered to spend and invest.

However, it’s essential to recognize that the Fed’s decisions will ultimately depend on economic data and global uncertainties. Should inflation rise or the economy show signs of stress, the Fed may reevaluate its approach. Therefore, while consumers can hope for further cuts, they should also remain vigilant and informed about potential changes in the economic landscape that could influence rates and borrowing conditions.

The Importance of Monitoring Economic Indicators

In the wake of the Fed rate cut, it’s crucial for both consumers and investors to keep a close eye on economic indicators. Understanding the trends in the labor market, inflation rates, and overall economic growth will be essential for making informed financial decisions. As these indicators fluctuate, they provide insight into how the Fed might adjust its policy in the future, impacting everything from mortgage rates to investment strategies.

Moreover, the interconnectedness of these indicators means that changes in one area can have ripple effects across the economy. For instance, a rise in unemployment could prompt the Fed to implement further rate cuts, while increases in inflation may lead to tightening policies. By monitoring these trends, consumers and businesses can better prepare for the financial implications of the Fed’s policies and navigate the complexities of the current economic environment.

Frequently Asked Questions

How does the Fed rate cut affect mortgage rates?

The recent Fed rate cut is likely to lead to lower mortgage rates, helping improve housing affordability. As the Fed continues to ease policy, borrowers can expect mortgage rates to decrease further, easing some of the financial burdens on home buyers.

What impact does a Fed rate cut have on credit card debt?

A Fed rate cut generally leads to lower interest rates on credit cards, which can provide consumers with relief from high credit card debt. However, it’s important to note that immediate changes may be slow to materialize, as credit card interest rates often lag behind changes in the Fed’s rates.

How will the Fed rate cut influence economic growth?

The Fed rate cut is designed to stimulate economic growth by making borrowing cheaper. This can encourage consumer spending and investment, helping to create more jobs and boost the overall economy in the following months.

Can the Fed rate cut improve housing affordability?

Yes, the Fed rate cut will likely contribute to lower mortgage rates, which can improve housing affordability for potential homebuyers. As borrowing costs decrease, more individuals may find it easier to afford homes.

When can consumers expect relief from high interest rates after a Fed rate cut?

Consumers may see some relief in high interest rates, but it might take time. While the Fed’s cut helps, other factors influence credit rates, meaning significant decreases in interest rates on loans, such as for credit cards and mortgages, may not happen immediately.

What does the Fed rate cut mean for future interest rates?

The Fed rate cut suggests that more cuts may be on the horizon. If economic conditions continue to change, additional cuts could be implemented, impacting all interest rates, including those for mortgages and credit cards, leading to further potential savings for consumers.

Will the Fed rate cut affect the stock market?

Yes, the Fed rate cut typically bolsters investor confidence, leading to potential increases in stock market performance. Lower interest rates can stimulate economic growth, encouraging investments in equities as borrowing costs decrease.

| Key Points | Details |

|---|---|

| Fed rate cut | The Federal Reserve cut interest rates by 0.5 percentage points, the first reduction in four years. |

| Impact on Consumers | Consumers with credit card debt, car loans, and home buyers will benefit from lower borrowing costs. |

| Future Rate Cuts | Fed Chairman indicated there may be more cuts, possibly totaling another 0.5 percentage points by year end. |

| Mortgage Rates | Mortgage rates are likely to decrease further as the Fed eases its policy. |

| Expectations on Debt Relief | While credit card rates are lower than their peak, significant relief might take up to a year. |

Summary

The recent Fed rate cut is set to benefit consumers significantly, though the exact timing and extent of these benefits may vary. The Federal Reserve’s move to lower interest rates aims to stimulate economic growth while supporting job creation. However, while mortgage rates are expected to decline with further easing, consumer relief on credit card debt may take longer to materialize. The implications of the Fed rate cut extend beyond Wall Street, signaling a positive change for Main Street as well.