The economic impact of climate change is emerging as one of the most pressing issues of our time, fundamentally reshaping how economies operate around the globe. Recent studies reveal forecasts significantly larger than earlier predictions, estimating that every additional 1°C rise in temperature could inflict a staggering 12 percent loss to global GDP. This drastic reality underscores the urgent need for effective climate change economics, prompting policymakers to not only consider the immediate fiscal repercussions but also long-term strategies to mitigate these effects. As we delve deeper into the social cost of carbon and explore decarbonization policy, the economic forecast of climate change paints a bleak picture that demands urgent attention and coordinated global action. It’s time to recognize that the climate crisis poses not just an environmental threat, but an economic one that could redefine our future prosperity.

Addressing the fiscal ramifications of shifting climate patterns is crucial as we grapple with the broader concept of climate-induced economic disruption. The interplay between rising global temperatures and shrinking economic outputs offers a lens through which we can examine effective climate action. With insights from recent analyses highlighting potential GDP losses, the need for sustainable growth strategies has never been greater. Emphasizing the importance of robust economic assessments and innovative policies, we can better understand how to navigate the complexities of climate change in the economic landscape. Ultimately, engaging with the financial implications of ecological degeneration is essential in crafting resilient economies that can withstand the impacts of a warming planet.

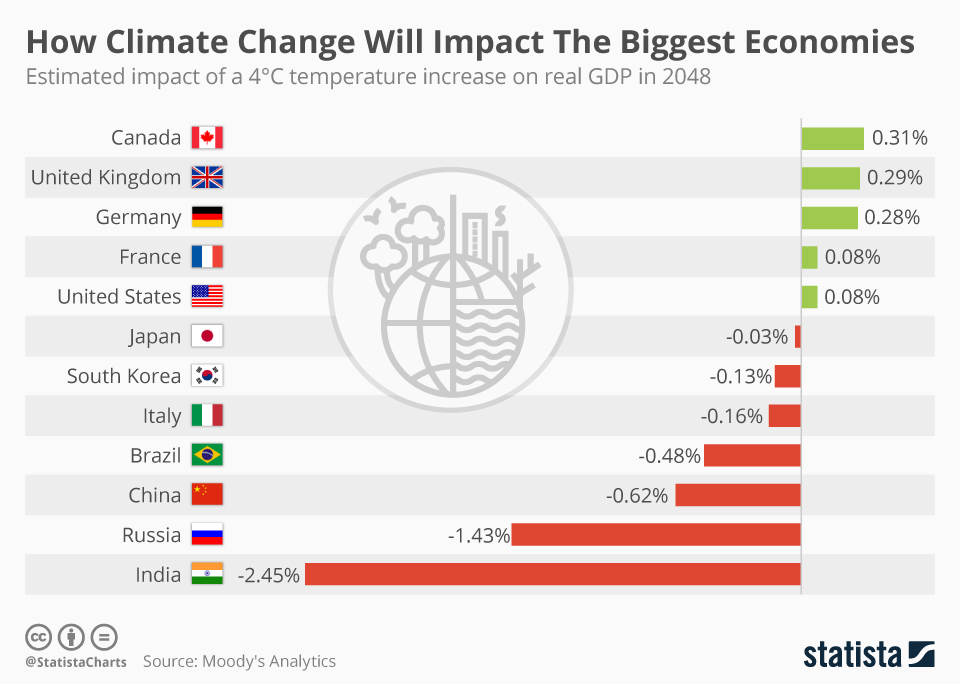

Understanding the Economic Impact of Climate Change

The economic impact of climate change is becoming increasingly evident in recent studies and projections. As global temperatures rise, the repercussions on economic performance are expected to be severe. Research indicates that each additional 1°C increase in temperature could lead to a staggering 12% decline in global GDP. These numbers represent a considerable escalation compared to previous estimates, highlighting the urgent need for effective climate policies that mitigate further warming.

The connection between climate change and economic fluctuations is complex. Traditional macroeconomic models have often underestimated the potential GDP loss due to climate shifts. However, advances in climate economics are now shedding light on the devastating impact on various sectors, especially agriculture and energy. As extreme weather events become more frequent and intense, the economic toll is likely to escalate, severely affecting productivity and long-term growth.

Revising the Cost of Climate Change

Given the alarming new consensus on the economic costs associated with climate change, revising how we calculate these impacts is critical. The use of historical weather data alongside economic records enables a more accurate assessment of the potential damages as temperatures rise. New methodologies propose that the conventional way of attributing economic loss based solely on local temperature data fails to account for the broader implications of global warming and its link to extreme weather patterns.

The findings of the study reveal just how necessary it is to rethink the financial ramifications associated with climate change. The projection suggesting that a 2°C increase would result in a 50% decline in output emphasizes the need for immediate action. There is a clear financial incentive for nations to embrace aggressive decarbonization policies, as the long-term costs of inaction could lead to losses far exceeding the upfront investment needed for greener technologies.

Decarbonization Policies: A Cost-Benefit Analysis

The urgency to implement decarbonization policies stems not only from environmental concerns but also from economic pragmatism. The latest analysis reveals a stark contrast between the benefits of investing in green technologies and the associated costs. The social cost of carbon, estimated globally at over $1,000 per ton, significantly outweighs the costs of interventions outlined in legislative actions like the Inflation Reduction Act. This presents a compelling argument for immediate and wide-ranging emissions reduction initiatives.

Furthermore, effective decarbonization can provide a pathway to sustainable economic growth. By investing in renewable energy and emissions-reducing technologies, nations can foster innovation that supports job creation and economic resilience. The economic forecast for countries that aggressively pursue these policies indicates not just a rebound in GDP but a potential doubling of wealth by 2100 if climate change is effectively curtailed.

The Role of Climate Change Economics in Policy-Making

The integration of climate change economics into policy-making is essential for crafting effective strategies to combat global warming. Economic analyses provide valuable insights into the potential costs and benefits associated with various climate initiatives. By quantifying the impacts of climate change on GDP and other economic indicators, policymakers can prioritize interventions that yield the highest returns on investment.

Furthermore, climate change economics empowers governments to anticipate and prepare for the potential fallout from warming temperatures. This proactive approach allows for the development of comprehensive strategies that not only focus on mitigation but also on adaptation, ensuring that economies can withstand the challenges posed by climate change. An informed economic perspective is crucial for rallying public support and securing funding for necessary climate action.

Exploring GDP Loss Due to Climate Change

GDP loss due to climate change is one of the harsh realities highlighted by recent research. As temperatures continue to rise, the projected economic toll reveals a critical shift in how analysts view the interplay between climate effects and national economic performance. The findings indicate a correlation between temperature rise and GDP decline, which underscores the urgent need for policymakers to consider these impacts in their strategic planning.

Understanding how GDP will be affected by ongoing climate change can guide investments in resilience and adaptation strategies. By projecting economic losses, nations can allocate resources effectively, focusing on sectors most vulnerable to climatic variations. This economic outlook illustrates that the costs associated with inaction can far exceed those of addressing climate change proactively and investing in sustainable technology solutions.

The Social Cost of Carbon: An Essential Metric

The social cost of carbon (SCC) serves as a cornerstone metric for evaluating the economic effects of greenhouse gas emissions. Recent studies suggest that the SCC is significantly higher than previously thought, which implies that current policies may be undervaluing the long-term damages associated with carbon emissions. By recalibrating this cost to reflect more accurate models and updated data, economists can make a stronger case for carbon pricing and other regulatory measures.

Accurately estimating the social cost of carbon not only aids in developing sound economic policies but also in legitimizing the need for collective action against climate change. The disparity between existing estimates and newer assessments shows a clear potential for greater returns on investment in climate action. Strong evidence highlights that mitigating emissions now could yield substantial economic benefits in the long run, establishing an economic rationale for urgent climate policies.

Long-term Economic Forecast Due to Climate Change

Climate change poses a significant threat to long-term economic stability, and recent forecasts paint a sobering picture. As the world grapples with rising temperatures and intensifying weather events, the potential disruption to economic growth is immense. Ensuring sustainable economic practices that can withstand climate impacts is crucial for future productivity and prosperity. The forecasts that predict increased GDP losses over time reveal a pressing need for integrative economic planning.

Incorporating climate risk into economic forecasts will allow governments to better prepare for adverse effects. Strategies that pivot towards greener technologies and sustainable practices could help mitigate these risks while enhancing economic resilience. With informed projections, we can begin shifting towards sustainable economic practices that prioritize the health of the environment alongside economic growth.

Technological Innovation: An Economic Lifeline in Climate Change

Investing in technological innovation is essential for addressing the economic challenges posed by climate change. As research suggests, advancements in green technology can drive down emissions and enhance productivity. By harnessing innovations like renewable energy, carbon capture, and energy-efficient infrastructure, economies can not only mitigate climate risks but also create new market opportunities that promote resilience and economic diversification.

Policymakers must recognize the dual role of technology in combating climate change and fostering economic growth. The proactive development of new technologies can lead to job creation in emerging sectors while simultaneously reducing the economic burden of climate impacts. Encouraging public and private investments in green technologies can lead to sustainable economic growth, emphasizing the importance of innovation in creating a better future.

Rethinking Climate Risk: Economic Implications

Rethinking climate risk involves understanding its profound implications for economic systems worldwide. The interconnectedness of global economies means that the effects of climate change in one region can have cascading repercussions elsewhere. As temperature increases and extreme weather events become more frequent, nations must adapt their economic strategies to cope with these realities.

Accepting and addressing climate risks in economic planning is crucial for ensuring long-term sustainability. Countries that take proactive measures to incorporate climate resilience into their economic strategies can gain a competitive advantage, safeguarding their progress against the inevitable impacts of climate change. Successful adaptation is not just about cost avoidance; it’s about seizing opportunities for growth in an increasingly complex global landscape.

Frequently Asked Questions

What is the economic impact of climate change on GDP?

Recent studies indicate that each additional 1°C rise in global temperatures could result in a 12% loss in global GDP. This projection represents a significant increase from earlier estimates, highlighting the severe economic repercussions of climate change.

How does climate change economics predict future economic conditions?

Climate change economics suggests that rising temperatures will continue to adversely affect economic conditions globally. By analyzing historical weather data and its correlation with economic output, researchers predict substantial GDP losses due to increased extreme weather events linked to climate change.

What is the social cost of carbon and its relevance to climate change economics?

The social cost of carbon quantifies the economic damages associated with each ton of carbon dioxide emissions. Recent calculations suggest a global social cost of $1,056 per ton, which underscores the significant economic impact of carbon emissions and supports the need for effective decarbonization policies.

How can decarbonization policy mitigate the economic impact of climate change?

Effective decarbonization policy can significantly reduce the social cost of carbon and minimize GDP losses associated with climate change. With cost-benefit analyses indicating that decarbonization strategies are economically viable, large economies like the U.S. can benefit from implementing these policies.

What are the long-term economic forecasts related to climate change?

Long-term economic forecasts related to climate change are concerning, projecting that failure to mitigate temperature rise could lead to a 50% decline in consumption and output by 2100. Such forecasts emphasize the urgent need for climate action to avert unprecedented economic consequences.

What role does technological innovation play in the economic impact of climate change?

Technological innovation can provide solutions to mitigate the economic impact of climate change, but it also contributes to emissions that exacerbate rising temperatures. Balancing these factors is crucial for developing effective climate change economics that prioritize sustainable growth.

How do extreme weather events correlate with economic productivity in relation to climate change?

Extreme weather events, which are rising due to climate change, negatively affect economic productivity by damaging infrastructure, disrupting markets, and increasing costs. Research shows that as global temperatures rise, the frequency and severity of such events also increase, leading to greater economic loss.

| Key Point | Details |

|---|---|

| Disconnect Between Predictions | Macroeconomists once predicted modest economic reductions due to climate change, while climate scientists warned of severe consequences. |

| New Economic Forecast | The recent study by Bilal and Känzig found economic impacts of climate change to be six times larger than previous estimates. |

| Impact on Global GDP | For each additional 1°C rise in temperature, there is a projected 12% decline in global GDP. |

| Future Implications | An additional 2°C increase could reduce global output and consumption by 50%. |

| Social Cost of Carbon | The global social cost of carbon is estimated at $1,056 per ton, significantly above earlier estimates of $185 per ton. |

| Decarbonization Benefits | Decarbonization strategies are cost-effective for large economies, showing strong benefits to economic policy. |

Summary

The economic impact of climate change is increasingly dire, as recent studies reveal that the projected costs are significantly greater than previously anticipated. A new analysis indicates that every 1°C increase in global temperature could lead to a devastating 12% decline in global GDP, emphasizing the urgent need for comprehensive climate policies. As temperatures rise, the potential losses become profound, potentially halving global output and consumption with a 2°C increase, reflecting impacts that surpass historical economic downturns like the Great Depression. Therefore, the economic ramifications are clear; addressing climate change is not merely an environmental necessity, but also an economic imperative.